One-Stop-Shop: Nicht kompatibel mit dem Handel auf Amazon & Co.

Update 27.05.2021: Die aktuellen Informationen zum One Stop Shop und den Auswirkungen für Amazon-Händler haben wir im OSS Wissenspool gesammelt.

Ab dem 1. Juli 2021 soll sich nach dem Willen der Mitgliedstaaten der EU die grenzüberschreitenden Umsatzsteuer-Compliance für Onlinehändler grundlegend vereinfachen.

Umfassende Gesetzesänderungen verbunden mit der Technologie des sogenannten One-Stop-Shop sollen den Binnenmarkt der EU von einer der letzten Hürden befreien: einem Umsatzsteuerrecht auf dem Stand des Jahres 1993.

In diesem Blogpost zeigen wir euch, dass diese Gesetzesreform dazu führen wird, dass es für viele Händler deutlich komplexer wird und Programme wie z.B. Amazon Pan EU neu gedacht werden müssen.

Fangen wir aber von vorne an.

Gesetzesänderung zum 1. Juli 2021

Disclaimer: Die im Folgenden erläuterte Gesetzesänderung wurde erst kürzlich um ein halbes Jahr verschoben – auf den 1. Juli 2021.

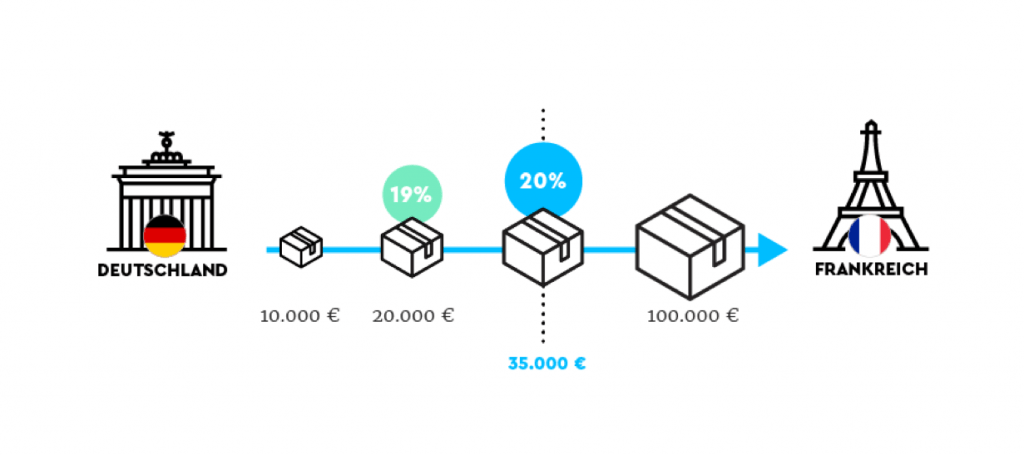

Im Rahmen der Neuregelung des § 3c UStG – welcher den Ort einer grenzüberschreitenden Lieferung in der EU an Privatpersonen regelt – werden die nationalen Lieferschwellen, wie sie in der folgenden Grafik dargestellt sind, wegfallen.

An die Stelle der nationalen Lieferschwellen tritt eine EU-weite Umsatzgrenze für grenzüberschreitende Lieferungen an Nicht-Unternehmer in der EU in Höhe von 10.000 Euro (netto).

Überschreitet ihr bzw. euer Mandant diese Grenze, unterliegen alle Lieferungen an Nicht-Unternehmer in der EU der Steuerpflicht im jeweiligen Bestimmungsland.

Das wird dazu führen, dass bereits jeder mittelgroße Händler in fast allen EU-Staaten steuerpflichtig sein wird, soweit er den grenzüberschreitenden Versand nicht deaktiviert.

Aus diesem Grund sollen Onlinehändler auf den sogenannten One-Stop-Shop (OSS) zurückgreifen können, welcher es ihnen ermöglichen soll, alle relevanten Ausgangsumsätze zentral über eine Schnittstelle – den OSS – in ihrem Heimatstaat zu melden.

Eine lokale steuerliche Registrierung in den einzelnen EU-Staaten wäre in diesem Fall nicht mehr erforderlich.

Die folgende Grafik verdeutlicht den Prozess – auch wenn in der Ausbaustufe des OSS zum 1. Juli 2021 zunächst nur B2C-Transaktionen über den OSS abgewickelt werden können.

Wie wir bereits im Jahr 2017 erläutert hatten, wird das nicht allen Onlinehändlern möglich sein.

Jeder Onlinehändler, der auch nur ein Fulfillment-Center im EU-Ausland nutzt, wird sich weiterhin lokal im EU-Ausland registrieren müssen.

Warum?

Grenzüberschreitendes Fulfillment by Amazon, Zalando, Cdiscount, …. versus OSS

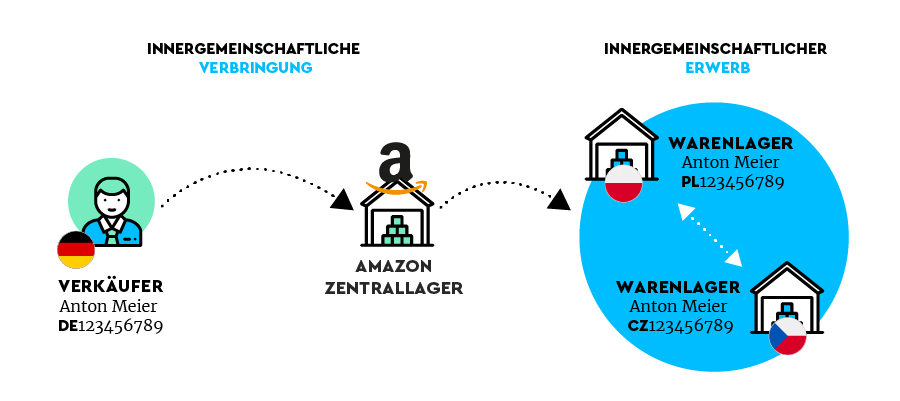

Die Verwendung grenzüberschreitender Fulfillment-Strukturen – z.B. Amazon Pan EU – führt dazu, dass aus umsatzsteuerlicher Sicht regelmäßig eine besondere Art von Transaktionen anfällt.

- Innergemeinschaftliche Verbringungen und

- Innergemeinschaftliche Erwerbe.

Diese Transaktionen führen wie in der Grafik beschrieben zu Steuer- und damit auch Registrierungspflichten im EU-Ausland.

Problem: Diese Transaktionen lassen sich nicht über den OSS melden, da es B2B-Transaktioen sind. Diese müssen weiterhin – nach einer lokalen Registrierung – durch die Abgabe lokaler Umsatzsteuer-Erklärungen deklariert werden.

Für viele Händler ändert sich also nichts – im Gegenteil: Umsatzsteuer-Compliance wird für die meisten einen noch deutlich größeren Platz einnehmen als bisher schon.

Sind vielleicht Gestaltungen, Workarounds, Vereinfachungen, …. denkbar?

Schauen wir uns drei Gedanken dazu an.

A. Kann man die i.g. Verbringungen lokal melden und den Rest über den OSS?

Ja, das ist möglich. Dazu müssen jedoch innerhalb des Unternehmens zwei Compliance-Stränge etabliert werden.

- Fernverkäufe über den OSS und

- alle anderen Transaktionen (lokale Verkäufe, Verbringungen, ….) über lokale Meldungen.

B. Kann man die Meldungen der i.g. Verbringungen einfach unterlassen?

Nein!

Werden die grenzüberschreitenden Warenverbringungen durch Amazon oder einen anderen Logistiker nicht gemeldet, unterliegen diese automatisch seit dem 1. Januar 2020 der Steuerpflicht.

Das bedeutet, ihr bzw. eure Mandanten müsstet für Warenverbringungen, für die niemals ein Geldeingang erfolgt, da es umsatzsteuerlich fingierte Umsätze sind, Umsatzsteuer abführen.

Kann man den OSS selektiv nutzen – also zumindest in Staaten, in denen man keine Fulfillment-Center nutzt?

C. Kann man dort, wo ein Fulfillment-Center verwendet wird, lokal melden und den Rest über den OSS?

Jein!

Der Gesetzesentwurf sagt zu dieser Frage (siehe § 18j Abs. 1 S. 4 UStG n.F.).

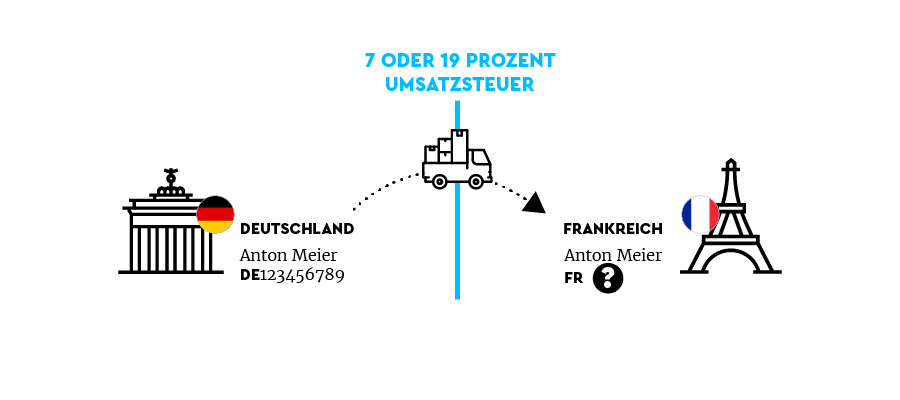

Eine Teilnahme an dem besonderen Besteuerungsverfahren – gemeint: OSS – ist nur einheitlich für alle Mitgliedstaaten der EU und alle Umsätze – hier gemeint die Lieferungen an Nicht-Unternehmer – möglich (…).

Das bedeutet: Grenzüberschreitende Lieferungen an Nicht-Unternehmer (sogenannte Fernverkäufe) müssen zwingend für alle EU-Staaten entweder vollständig über den OSS oder vollständig für alle EU-Staaten lokal gemeldet werden.

Drastische Konsequenzen – im worst case: Registrierungspflichten in fast allen EU-Staaten und Probleme für Amazon & Co.

Das wird dazu führen, dass Händler, die ein grenzüberschreitendes Fulfillment nutzen – z.B. Amazon CEE oder Amazon Pan EU – sich in jedem Staat steuerlich registrieren müssen, in den sie auch nur ein Paket an Nicht-Unternehmer schicken, wenn sie es nicht schaffen, zwei Compliance-Stränge zu etablieren: Fernverkäufe über den OSS und alles andere lokal zu melden.

Für einen Marktplatz wie z.B. Amazon, der seine Marktplatzhändler regelmäßig motiviert, ihre Produkte EU-weit zu lagern und diese Kapazitäten laufend ausbaut, kann das zu einem erheblichen Problem werden. Der Marktplatz lebt hervorragend von Fulfillment-Gebühren und Vertriebsprovisionen.

Sollten sich viele Händler aufgrund der o.g. Konsequenzen nun überlegen, ihre Aktivitäten herunterzufahren, wäre das für den Giganten ein erheblicher Einschnitt in Europa – dank einer Gesetzesreform, die Gutes bewirken sollte aber überwiegend das Gegenteil bewirkt.

Taxdoo ist die Compliance-Plattform für die digitale Ökonomie

… und bildet für die führenden Onlinehändler in Europa neben der Abwicklung der laufenden EU-weiten Umsatzsteuer-Compliance, Intrastat und Finanzbuchhaltung (Taxdoo ist Partner der DATEV) noch zahlreiche weitere Compliance-Services über eine einzigartige Plattform ab.

Wenn ihr mehr darüber wissen wollt, wie ihr Umsatzsteuer-Compliance, Finanzbuchhaltung und noch viel mehr effizient und sicher über eine Plattform abbilden könnt, dann bucht über diesen Link euer individuelles und kostenloses Erstgespräch mit den Compliance-Experten von Taxdoo!

Gerne könnt ihr euch auch für unser regelmäßig stattfindendes Demo-Webinar anmelden, in dem wir euch Taxdoo und unsere Compliance-Services vorstellen und eure Fragen persönlich beantworten.

Weitere Beiträge

OSS-Meldungen für Q1-2024 abgelehnt, weil Steuersätze beim BZSt nicht up to date sind.

OSS-Mahnungen aus Spanien für Q3 und Q4 2021: BZSt dieses Mal nicht Schuld

Reverse-Charge: Wann zahlt Ihr die Umsatzsteuer für Amazon, TikTok und Co.? Ein aktuelles BFH-Urteil!